Key Reasons for a CPA to Take An Advocacy Role

2016 Final DOL Rule: “The changes in the retirement landscape over the last 40 years have increased the importance of sound investment advice for workers and their families. While many advisers do act in their customers’ best interest, not everyone is legally obligated to do so. Many investment professionals, consultants, brokers, insurance agents and other advisers operate within compensation structures that are misaligned with their customers’ interests and often create strong incentives to steer customers into particular investment products. These conflicts of interest do not always have to be disclosed and advisers have limited liability under federal pension law for any harms resulting from the advice they provide to plan sponsors and retirement investors. These harms include the loss of billions of dollars a year for retirement investors in the form of eroded plan and IRA investment results, often after rollovers out of ERISA protected plans and into IRAs.”

Source: DOL Fiduciary Final Rule 4/2016

What are the key reasons for the CPA to take an advocacy role?

Plan sponsors, as a whole, are unaware that participants pay disparate fees, and service providers, particularly record-keepers that receive revenue-sharing payments, are not going to address it, experts say. It is incumbent on sponsors, then, to ask their plan advisers and record-keepers about fee levelization.

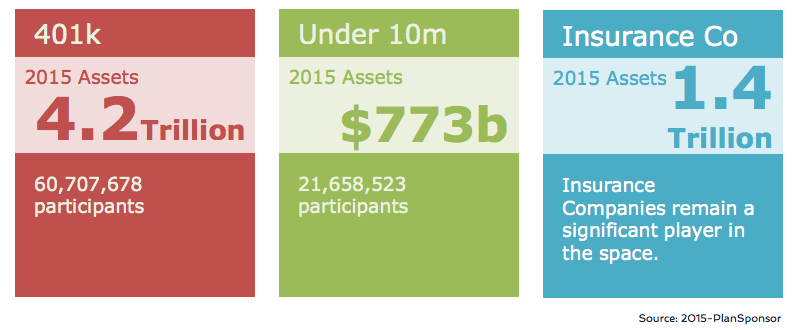

January 14th, 2016-PlanSponsor

The tax professional is in a unique role as a trusted advisor to a business owner. The broker or advisor to a retirement plan has no incentive to review their own fees. Certainly, the recordkeeper or 401k platform provider is not going to raise the issue of their own fees with the business owner. Uniquely, the CPA, EA, or plan auditor is. Understanding the key points made in the DOL is an imperative for the tax professional that advises business owners.

Understanding the key points made in the DOL is an imperative for the tax professional that advises business owners.

The DOL makes two main points:

• Plans are paying excessive fees.

• Plan sponsors need a mechanism to identify and deal with conflicts of interest.

Leave a Reply

Want to join the discussion?Feel free to contribute!