Adding client value by effectively communicating the momentous and substantial sea-shift promulgated by the Department of Labor’s “Fiduciary Rule” legislation.

As accounting professionals turned their after-Labor Day focus to meeting corporate tax extension deadlines attention is also being given by practitioners to making the follow-up communication to the client on their tax and business planning considerations impactful and actionable.

We would like to suggest that one timely and quick way to accomplish this is to add a paragraph or two that extends the conversation to the client’s retirement plan.

Points To Make

The DOL Fiduciary rule makes two main points with respect to 401k plans; fee’s matter, and conflicts of interest matter.

Both fee structure and conflicts of interest are clear responsibilities of the plan sponsor, which is your business client. In this new environment, tax professionals should be aware of the increased need to review plan structure, and the initial review can start with the 408(b)(2) form.

The basic requirements of the fiduciary is to act in the best interest of the plan participants and make prudent decisions on behalf of the plan, which included the investment performance, risks, and costs, and the type and amount of services provided to the plan.

As background, the 408(b)(2) regulation requires that service providers make disclosures about services, compensation, and fiduciary status. That’s the starting point. The law then requires that the plan sponsor fiduciary evaluate those disclosures and determine whether the compensation is reasonable in light of the services. Usually, that requires benchmarking against industry averages for similar providers and comparable services.

Most business owners don’t even realize that they are the “fiduciary” in question.

Pity the business owner who is now aware of this exposure and his corresponding realization that he or she doesn’t have the information to fulfill his or her fiduciary responsibilities. While there may be exceptions, it would be difficult for a business owner to evaluate compensation of its service providers if it hadn’t calculated the amount of that payment, including indirect compensation such as 12b-1 fees and sub-transfer agency fees. For those fees, a business owner would need data about how the amounts were calculated and who was paid. In other words, a business owner should already have that material in its due diligence file. Also, a business owner should have some industry information about the compensation of similarly situated service providers. The due diligence file should contain benchmark information for both types of providers. A key is to focus in this review are asset-based recordkeeping charges.

There is a lot for the client to consider. Recordkeeping is a good place get them started.

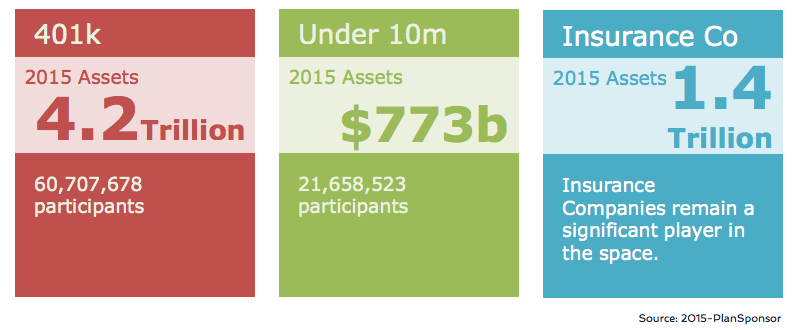

A good place to start your clients is to help them with understanding the recordkeeping aspect of their plan which includes services such as statements, participant websites, contribution source accounting, performance reporting, loan and distribution accounting. Many small and medium sized plans pay for recordkeeping services through an additional contract or asset based fee that is paid by participants. This type of fee is typical in insurance company provided plans.

Clients can best understand the impact of asset based recordkeeping fees by realizing that services do not scale with asset size, but the fee does.

A plan with a .25% annual recordkeeping charge or asset based fee deducts $250 for services from a participant with $100,000 balance and $25 from a participant with a $10,000 balance. The services delivered are the same. Another way to look at the cost of the fee is the compounded negative effect it has on retirement balances.

A fund that returns 10% is reduced to 9.75% as a result of this fee. A plan that has a high disparity of account balances- typical in professional services companies- the owner may unknowingly be paying significantly more than they think. They are likely not using the website, and just throwing their statements away. An annual review of these services and charges on the 408 (b)(2) statement will reveal areas of concern.

Are your client’s overwhelmed by this? Let them know accounting professionals can really help.

Let’s start with the most common situation. A business owner hasn’t reviewed the 408(b)(2) disclosures, hasn’t obtained benchmarking information and hasn’t evaluated the compensation of its service providers. Obviously, that’s a problem.

We believe that the best course of action would be for the CPA or tax professional to lead that discussion prior to corporate tax filing and tax prep services filing deadlines.

The business is typically looking risk reduction and cost savings advice during these review sessions. If a business owner goes through that initial process with the tax preparer and requests the 408 (b)(2) statement, the and decides that the costs are—and were—reasonable, then, while there may have been a fiduciary failure by not having done it earlier, at least the members will know there had been no damages—the plan and participants hadn’t been hurt by making excessive payments and conflicts of interests were resolved.

A CPA suggesting this approach would be doing their clients a valuable service and would continue to cement the client’s impression of the CPA as one of a business owners must trusted advisors.

For some CPAs this could translate into some more billable hours and we would be glad to provide those CPAs with training on how to do this. For others that don’t have a desire or ability to do this in-house we would be happy to provide this service to the client on an outsourced basis. We can even help with a draft letter for you to send to your clients.

Want To Take A Deeper Dive?

Attached here you will find an overview of how Axxcess Link can help you with your CPA practice.

Please feel free to reach out to us to let us know how we can help.